To pivot their portfolio companies toward growth, PE firms have relied on a variety of tools to survive a global recession and the shift to a remote work environment. From capital injection, to restructuring process assistance, to technology deployment, firms are working with their portfolio companies to maintain market relevance.

Of course, private equity has rarely been in a better position resource-wise to support their portfolio. Preqin reported PE was sitting on a record-setting US$1.46 trillion of dry powder, which was critical in drafting new strategies for their portfolio companies to come out on the other side of the pandemic stronger.

Moreover, compared to the 2008 crisis, the private lending market is three times larger and more mature, according to investment manager firm Alvarium Investments. This growth enabled it to fill the gap left by banks getting cold feet over strong investments amid the prevailing uncertainty triggered by the virus.

As per S&P’s PE Mid-Year Survey on a global scale published in September 2020, PE firms expect to focus their efforts on making new, selective investments and stabilizing their current portfolio while fundraising seems to be on the backburner going forward. How are private equity investors executing these offsetting efforts, and how will these strategies help their portfolio become more resilient to future market changes?

War room strategies: Private Equity’s arsenal to tackle portfolio challenges

The pandemic posed major health and business disruptions, calling for business reinvention. It also erected substantial barriers to deal execution and valuation shifts for PE firms. Covid-19 also unveiled business model chinks within their portfolio companies.

In the medium term, finance expert Natasha Ketabchi anticipates PE funds will do one of three things:

- Retrench into local markets and capitalize on established public policy incentives in place to weather the storm.

- Deepen their sector specialization to become niche specialists in sectors that thrived despite the pandemic.

- Move strategically based on the achieved EBITDA margins through a combination of dry powder use and flexibility buildup.

On the long-term front, Alvarium Investments anticipates stability and resilience will trump growth for PE’s portfolio companies, prioritizing cash-flow generation over cash flow drains.

PE firms have set up “cash war rooms“

Cash war rooms are beneficial to companies facing liquidity issues and dampened demand. They focus on three particular tasks:

- Speeding up risk valuations and detecting potential savings.

- Identifying cash levers

- Collaborating with business leaders and outside experts.

The cash war room can operate remotely as long as it maintains a constant line of communication between the companies’ CFO, treasurer, and executive group. Through digital tools, a centralized dashboard showing the corporate balance sheet and cash-flow diagnostics can be designed and rolled out in real-time, to fast-track decision-making.

The war room’s ultimate goal is to achieve operational normalcy amid uncertainty. PE firms need to prevent their portfolio companies from shrinking their investments throughout the downturn — a lesson learned during the financial downturn of 2008. They also help portfolio companies tailor product and service offerings to their clients, to redesign contract structures to consolidate customer loyalty, and to get ready for M&As.

Spend control towers keep expenses in check

While the war room primarily serves the need to preserve liquidity, PE firms are also implementing “Spend Control Towers” (SCT) to make good on their portfolio companies’ commitment to deliver savings as they navigate the Covid-19 tide.

Usually designed to operate in a fixed period ranging between six to 12 months, an SCT is a centralized decision-making body where expense needs are pitched by a company’s managers. The result is a streamlined savings process. While an SCT does not manage the direct costs of goods sold, it oversees virtually everything else, including point-of-sale purchases, invoices, expense reports, and recurring expenses.

This approach is not without its inherent challenges as its reach goes beyond modifying processes and behaviors; SCTs may even look to change mindsets and culture around budgets and expenditures. To be successful, SCT teams require unclouded top-down mandates as well as unequivocal engagement of senior management.

Regional distinctions in private equity firms’ Covid-19 portfolio response

The European PE market outperformed the rest of the world in 2019. Benelux, Nordic, and UK LBO funds delivered the strongest returns among European countries last year, delivering IRRs of 16.64 percent, 16.29 percent, and 15.6 percent, respectively.

Funds in DACH nations—Germany, Austria, and Switzerland — saw sharp performance improvements, with an IRR of 10.9 percent, up from 5.8 percent for the prior year.

This continued into June 2020, with primarily European PE firms showing the continent’s high spirits, despite the impacted revenue forecasts and paused exit strategies.

Looking to 2021, the optimism continues — 74 percent of surveyed PE firms stated they were open for business and looking for new investment opportunities in the immediate term, and 61 percent were bullish on returning to business as usual by 2021.

By September 2020, the region was on track to deliver a commendable performance, albeit not to last year’s levels. Public aid programs for businesses, paired with quick government action to impose early lockdowns were instrumental in the recovery.

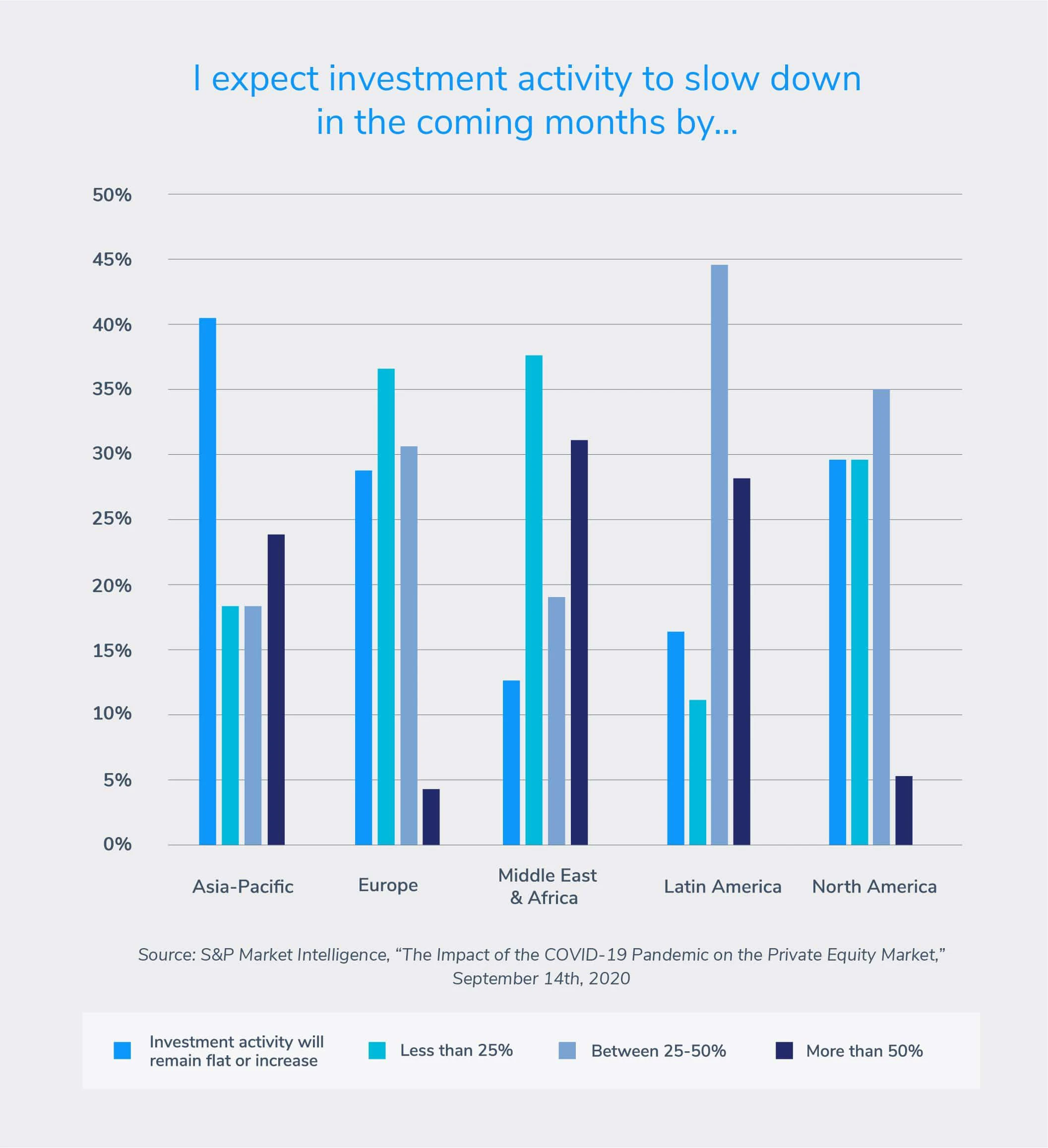

Asia-Pacific investors come out as the most optimistic among the PE firms surveyed in S&P’s Mid-Year PE Survey. Forty percent anticipate a positive outlook when considering a post-Covid landscape.

The optimism may be rooted in the fact that Asia was the first to deal with the virus, making the region a frontrunner in the road toward recovery, witnessing a mild uptick in investments.

S&P Global Market Intelligence data found PE and VC entry value in the APAC region increased by 31 percent, from US$23.7 billion in 1Q20 to US$31.2 billion in 2Q20.

The 22 percent of respondents that anticipated a hampered investment activity by 50 percent may be linked to India’s prevalent difficulties in handling the pandemic.

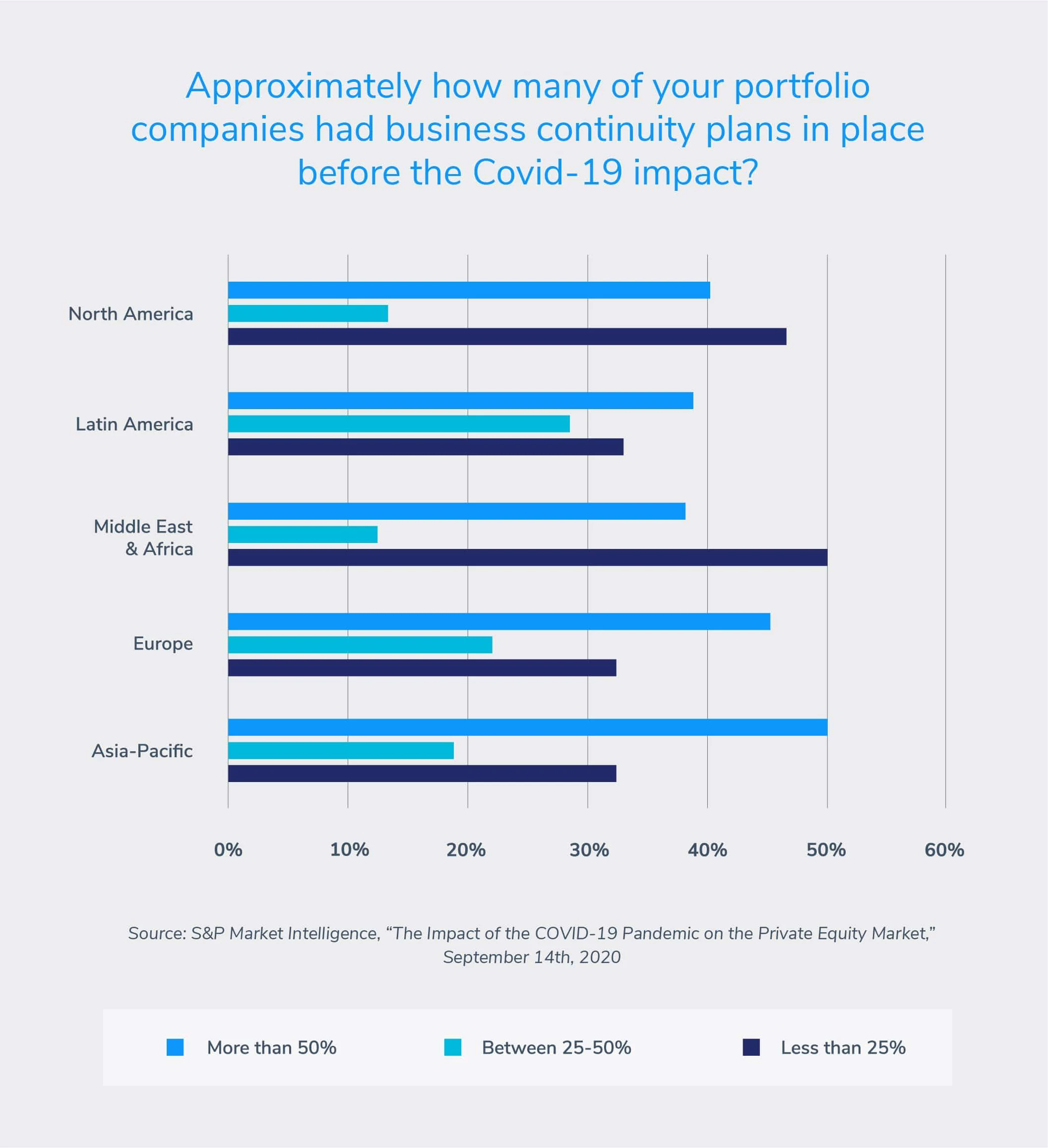

PE firms must have business continuity plans established to secure future resiliency across their portfolio companies. S&P’s survey found that, on average, 40 percent of surveyed firms signaled more than half of their portfolio companies had business continuity plans in place before the Covid-19 outbreak.

APAC respondents reported the highest percentage at 50 percent. This might be a result of the region’s previous experience battling local epidemics.

By contrast, North American-based portfolio companies were the least prepared for severe business disruptions. Forty-six percent of North American PE firms reported that less than 25 percent of their portfolios had business contingency plans ready. The survey stresses the need for the design and implementation of sturdy business strategies toward growth, sustainability, and resiliency.

Drive strategic growth

Add value to your portfolio — leverage the right partners to help portfolio companies succeed, even in uncertain economic times. Download our guide to driving strategic growth to learn more about how we can help.