为了使投资组合公司转向增长,常设机构公司依靠各种工具来度过全球经济衰退和向远程工作环境的转变。 从注资、重组流程协助到技术部署,各公司都在与投资组合公司合作,以保持市场相关性。

当然,私募股权在资源方面很少有更好的位置来支持他们的投资组合。 Preqin报道常设机构坐拥创纪录的美元1 。 46 他们拥有数万亿美元的可用资金,这对于制定投资组合公司的新战略至关重要,以便这些公司能够从疫情中走出来,变得更加强大。

此外,据投资管理公司 Alvarium Investments 称,与2008危机相比,私人借贷市场规模扩大了三倍,也更加成熟。由于疫情引发的不确定性,银行对强劲的投资犹豫不决,而这种增长使它能够填补由此留下的空白。

根据标普9月发布的全球常设机构年中调查报告2020 ,常设机构公司预计将把精力集中在进行新的、有选择的投资和稳定其现有投资组合上,而筹资似乎在未来会被搁置。 私募股权投资者如何执行这些抵消措施?这些策略将如何帮助他们的投资组合更具抵御未来市场变化的能力?

作战室战略:私募股权投资公司应对投资组合挑战的武器库

疫情对健康和商业造成了重大冲击,需要企业进行转型。它还为常设机构公司的交易执行和估值调整设置了实质性障碍。 Covid- 19还揭示了其投资组合公司内的商业模型漏洞。

金融专家娜塔莎·凯塔布奇 (Natasha Ketabchi)预计,中期内,常设机构的资金将采取以下三种做法之一:

- 收缩到当地市场,利用现有的公共政策激励措施来抵御风暴。

- 深化部门专业化,成为在大流行病中仍能蓬勃发展的部门的利基专家。

- 通过结合使用干粉和提高灵活性,在实现 EBITDA 利润率的基础上进行战略调整。

从长远来看,Alvarium Investments 预计,对于常设机构的投资组合公司而言,稳定性和韧性将胜过增长,优先考虑现金流的产生而不是现金流的消耗。

常设机构公司设立“现金作战室”

现金作战室有利于面临流动性问题和需求减少的公司。他们重点关注三项特殊任务:

- 加快风险评估,发现潜在的节约潜力。

- 确定现金杠杆

- 与企业领导和外部专家合作。

只要在公司的首席财务官、财务主管和执行小组之间保持持续的沟通,现金作战室就可以远程运作。通过数字工具,可以设计并实时推出显示企业资产负债表和现金流诊断的中央仪表板,以快速做出决策。

作战室的最终目标是在不确定性中实现作战正常化。常设机构需要防止其投资组合公司在经济低迷时期缩减投资——这是在2008金融危机期间吸取的教训。 他们还帮助投资组合公司根据客户需求定制产品和服务,重新设计合同结构以巩固客户忠诚度,并为并购做好准备。

支出控制塔控制支出

虽然作战室主要服务于保持流动性的需要,但常设机构公司也在实施“支出控制塔”(SCT),以履行其投资组合公司在应对 Covid 19浪潮时实现节约的承诺。

SCT 通常设计为在 6 到12月的固定时间内运作,它是一个集中决策机构,公司经理会在此提出费用需求。最终实现的是简化储蓄流程。虽然销售成本控制员不直接管理销售商品的成本,但它几乎负责管理其他所有事项,包括销售点采购、发票、费用报告和经常性支出。

这种方法并非没有固有的挑战,因为其影响范围不仅限于修改流程和行为;小规模技 术项目甚至可能寻求改变围绕预算和支出的思维方式和文化。要取得成功,SCT 团队需要明确的自上而下的指令以及高层管理人员的明确合作。

私募股权公司应对新19疫情的投资组合策略存在区域差异

欧洲常设机构市场在2019表现优于世界其他地区。 去年,比荷卢、北欧和英国的 LBO 基金在欧洲国家中回报率最高,内部收益率分别为16.64 %、16.29 % 和15.6 %。

德国、奥地利和瑞士8三个德语区国家的基金业绩大幅提升, 9 10 ,高于上一年的5 %。

这种情况一直持续到 6 月2020 ,尽管收入预测受到影响,退出策略也暂停,但主要以欧洲常设机构公司为主,展现了欧洲大陆的高涨情绪。

展望2021 ,乐观情绪仍在继续—— 74 % 的受访常设机构公司表示,他们正在营业,并在短期内寻找新的投资机会, 61 % 的公司对2021恢复正常营业持乐观态度。

到9 月2020 ,该地区有望取得令人满意的成绩,尽管没有达到去年的水平。政府对企业的公共援助计划,加上迅速采取早期封锁措施,对经济复苏起到了至关重要的作用。

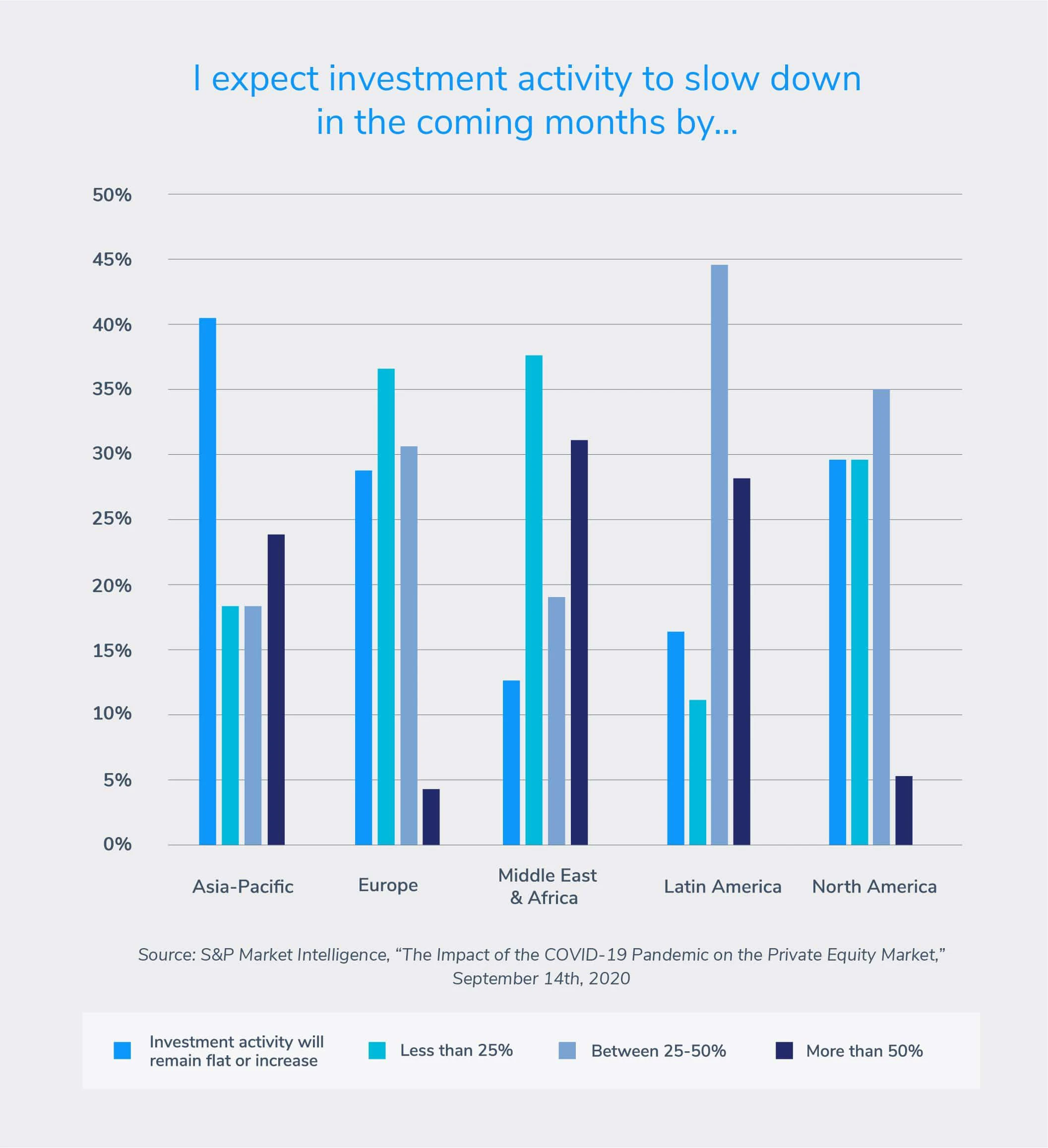

在标准普尔年中常设机构调查中,亚太地区投资者是接受调查的常设机构公司中最乐观的。 40%的人对后疫情时代的前景持乐观态度。

这种乐观情绪可能源于亚洲率先应对病毒,使该地区成为复苏道路上的领跑者,见证了投资的温和增长。

标普全球市场情报数据显示,亚太地区的常设机构和风险投资进入额增长了31 %,从1季度20 7亿美元23到2季度20 31 2美元。

22 % 的受访者预计投资活动将受到阻碍,这一比例为50 %,这可能与印度在应对疫情方面普遍存在的困难有关。

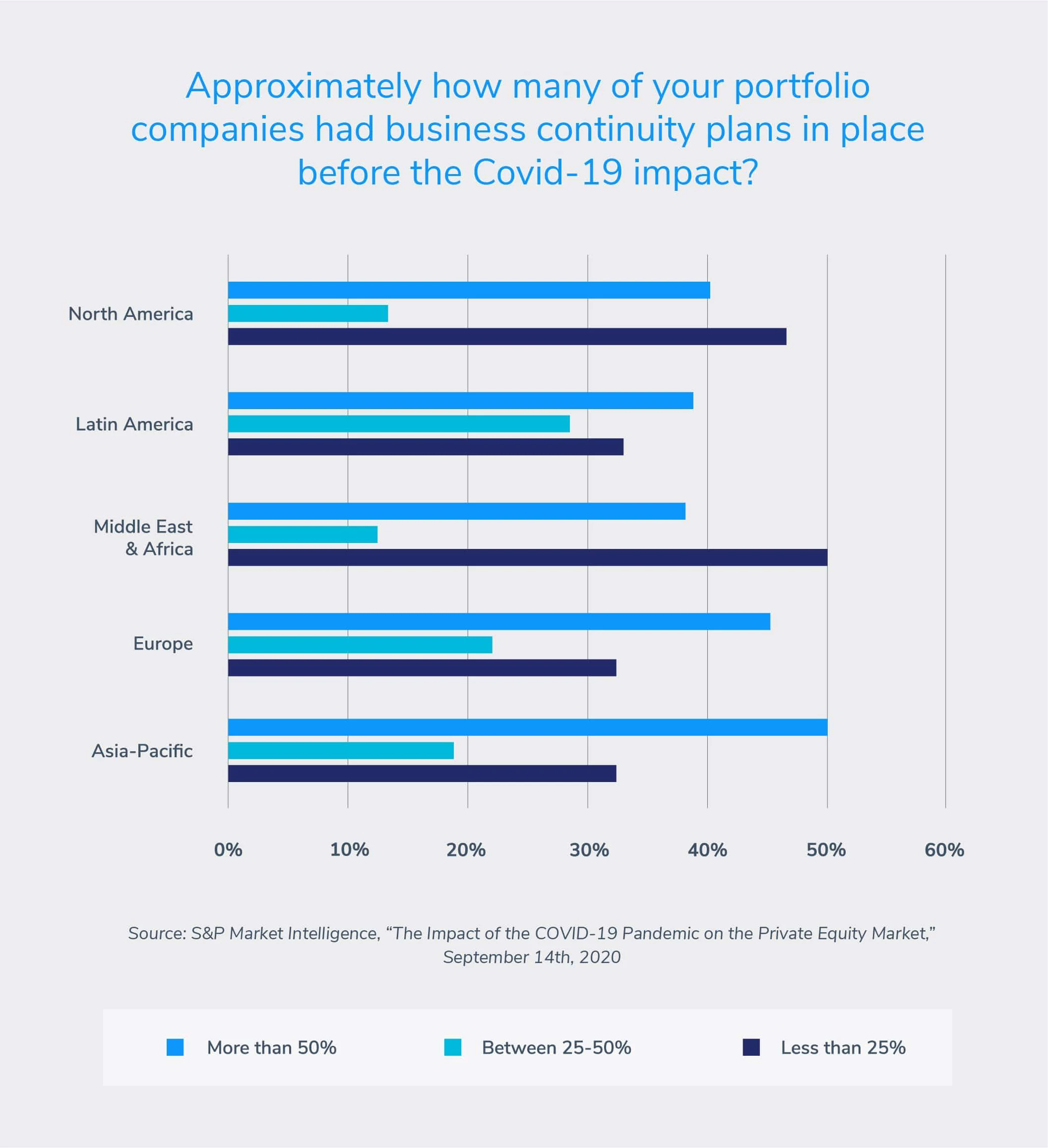

常设机构必须制定业务连续性计划,以确保其投资组合公司的未来韧性。 S&P 的调查发现,平均而言,40 %的受访公司表示,在 Covid-19 爆发之前,他们所投资的公司中有一半以上已经制定了业务连续性计划。

亚太地区受访者报告的比例最高,为50 %。这可能是该地区此前应对地方性流行病的经验所致。

相比之下,总部位于北美的投资组合公司对严重的业务中断准备最不足。46% 的北美常设机构公司报告称,其投资组合中不到25 % 的公司已准备好业务应急计划。 该调查强调了制定和实施稳健的商业战略以实现增长、可持续性和韧性的必要性。

推动战略增长

为您的投资组合增值--利用合适的合作伙伴帮助所投资的公司取得成功,即使在经济形势不明朗的时期也是如此。下载我们的战略增长驱动指南,了解我们如何为您提供帮助。