A workplace pension scheme allows employees to save towards their retirement with the help of their employer. Since 2016, the workforce pension plan has improved drastically, with employer pension contributions increasing from just 1 percent to now 4 percent of each employee’s salary.

Employers must now also pay a minimum contribution of 3 percent as of April 2019. These contributions go towards the employee pension pot and allow your employees to save more towards their retirement.

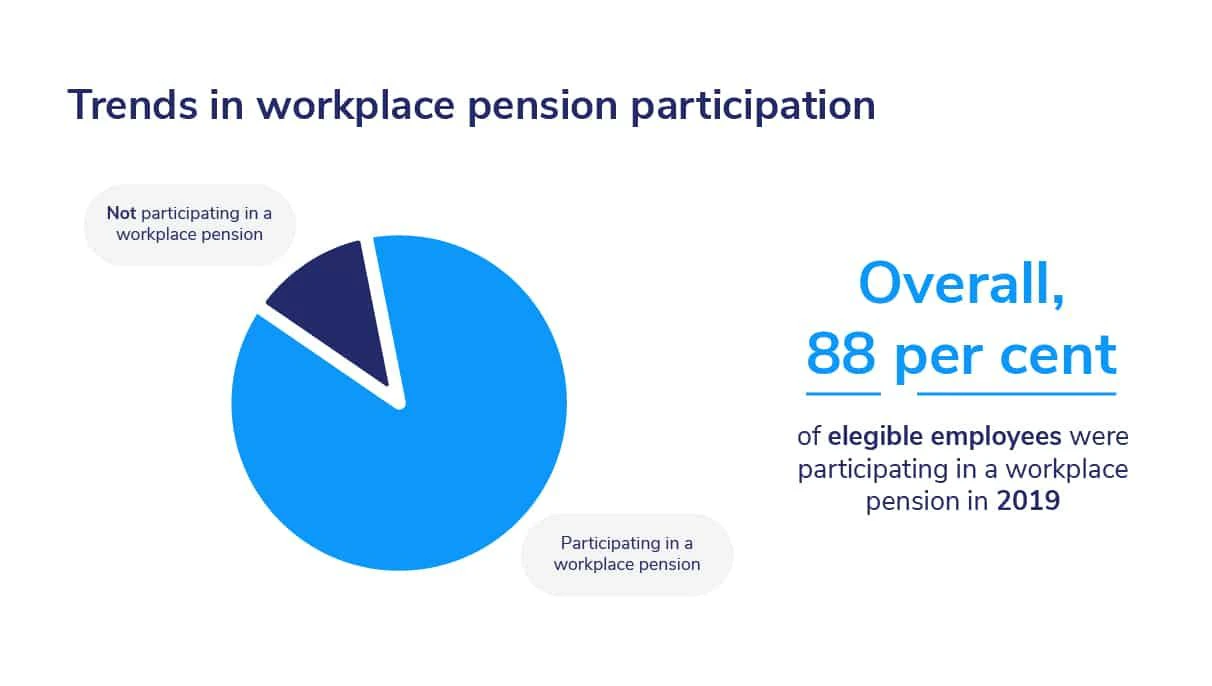

Trends in workplace pensions

According to the Annual Work & Pensions Report 2009 – 2019, participation in workplace pensions has increased in private and public sectors. Overall, a massive 88 percent of eligible employees participated in a workplace pension in 2019. This indicates the positive impact of the workplace pension reforms to date and the implementation of automatic enrollment.

Additionally, enrollment in workplace pensions has increased across different employer sizes. For example, in the public sector, since 2014, participation rates have increased steadily, with small employers (5 to 49 employees), as well as larger employers.

In the private sector, 2019 saw substantial growth for the larger employers (5000+ employees), with 91 percent of eligible employees participating in workplace pension schemes. The UK government has rolled out other significant updates to the pension plan; for example, before 2012, only the larger employers were required to participate. Fast-forward to 2017 and beyond, and all UK employers, regardless of size, are required to provide a compliant workplace pension scheme.

As an employer, it is vital to stay up to date with the latest workplace pension trends. However, what’s even more important is knowing the four critical steps for providing a pension plan in the UK.

1. Choose a pension scheme

- Choosing a pension scheme for your employees can be a challenging feat, but there are several vital factors to consider:

- Determine whether you are able to offer automatic enrollment to employees who want to participate in the pension scheme. Specific criteria need to be met to qualify for automatic enrollment, like the number of staff and various entry requirements.

- Identify and prepare for all associated costs.

- Ensure you have set up your pension plan to work seamlessly and compliantly with your payroll system, and that you secure the necessary expertise to support you throughout the process.

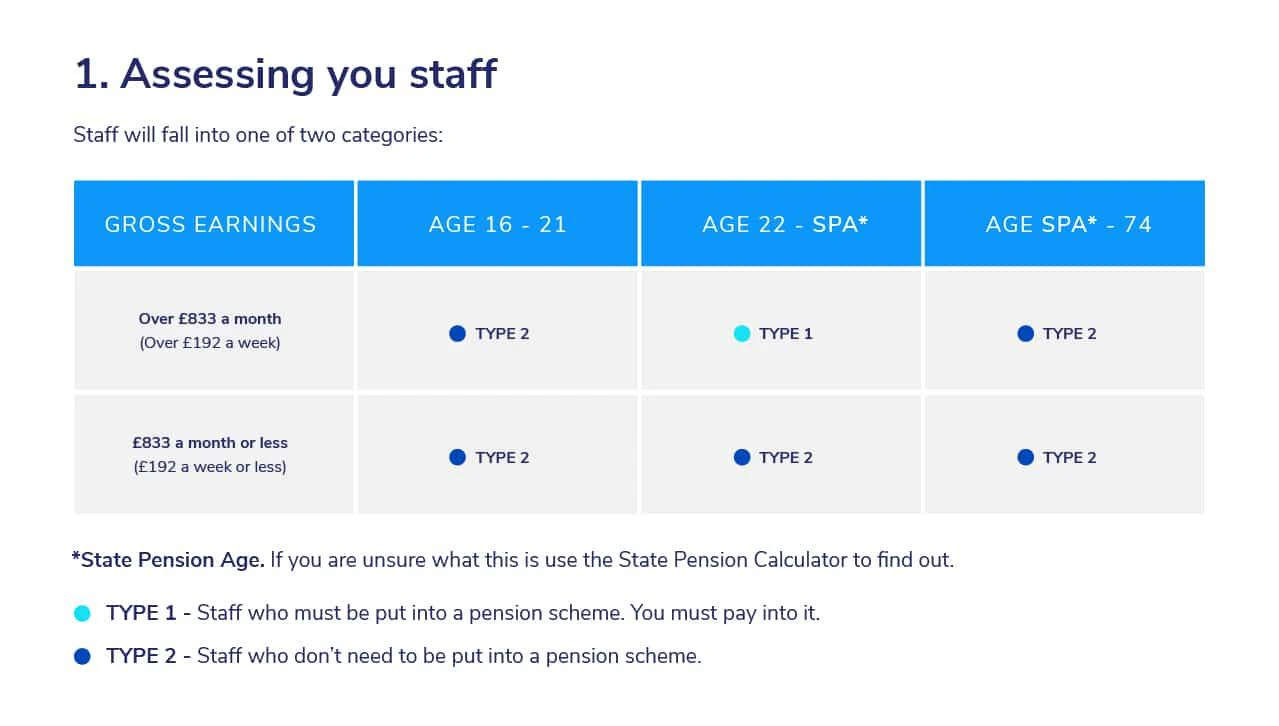

2. Determine who qualifies for the workforce pension scheme

This step is known as “assessing your staff.” Usually, employers are advised to do this on their “duties start date,” which is the day the first member of your team starts work. To understand which of your employees qualify for the workplace pension scheme, you must work out specific criteria, such as how much each employee earns, how old they are, and the pension contribution rates.

To do this easily, your team will generally fall into one of the two categories:

Type 1: Employees who must be put into a workplace pension scheme because they earn over 10,000 British pounds per year and are between 22 years old and the SPA (State Pension Age). To calculate the SPA, use the State Pension Calculator, which can be found on the UK government website. As an employer, you must pay into it (this will go towards the employee pension pot).

Type 2: Employees who do not need to be put into a workplace pension scheme. These employees choose to join your pension scheme; however, as their employer, you do not need to pay into it.

You must also consider your part-time employees and contractors. Assess whether you need to put these team members into the scheme and determine the contribute rate for each worker, as rates may vary.

Throughout this process, you also need to provide all the relevant employee information to your pension scheme provider. Once you have identified the employees who qualify for your workplace pension, you need to officially inform them.

3. Provide written clarification to your team

It is your legal duty to provide a written explanation for each participant that details the pension scheme process. Usually, employers in the UK are advised to do this six weeks after their duties start date. It is also important to contact your workplace pension provider if any additional information should be included in these letters.

4. Establish a declaration of compliance

One of the final and most critical steps is declaring your compliance. Employers need to declare their compliance within five months after their duties start date. Failure to do so could result in fines.

How can you declare your compliance and avoid getting fined? As an employer in the UK, you have to make sure all workplace pension-related forms are completed on time and all the information entered is correct and up to date.

Your UK workforce pension streamlined

Feeling a bit overwhelmed? We don’t blame you. Setting up a compliant and up-to-date UK workforce pension scheme can be a time-consuming and complex process. Researching, managing, and contracting with a pension provider can be challenging for companies to do on their own. Additionally, it adds tremendous overhead costs to in-house HR teams.

However, this should not stop you from hiring in the UK or internationally.

Our comprehensive global Employer of Record (EOR) solution enables our customers to hire in 187 countries without the need to set up costly international subsidiaries.

How can our EOR platform help you? Using Globalization Partners to hire your team in the UK, you can rest assured that we will take care of your workforce pension plan, making it a seamless part of your employee benefits package while reducing the workload for you and your team.

We invite you to contact us today, so we can aid you in onboarding UK employees, quickly and worry-free.