主なポイント:

- スタートアップの「死の谷」の定義: 「死の谷」とは、スタートアップが事業を開始したものの、まだ収益を上げていない期間のことです。

- 資金調達戦略:ベンチャーキャピタリスト、エンジェル投資家、オンラインプラットフォームから資金を確保し、安定した予算を維持する。

- スタートアップの成長のためのグローバル採用:国境を越えた採用は、多様な人材プールへのアクセスを可能にし、長期的な成功のための市場機会を拡大します。

- 雇用主記録 (雇用代行業者(EOR)) を使用してグローバルな雇用を簡素化: G-Pのような雇用代行業者 (EOR) と提携することで、事業体を設立することなく、 180か国以上のスタートアップ企業の雇用を支援します。

多くの企業は、いわゆるスタートアップの「死の谷」と呼ばれる時期に倒産する。しかし、この重要な局面とは一体何なのか、そして起業家はどのようにして「死の谷」を乗り越えることができるのだろうか?世界経済の逆風により、今日のスタートアップ市場はかつてほど活気に満ちていないかもしれないが、それでもなお、より良いスタートアップを明日築くために、初期段階で直面するであろう課題を今こそ理解しておく絶好の機会である。

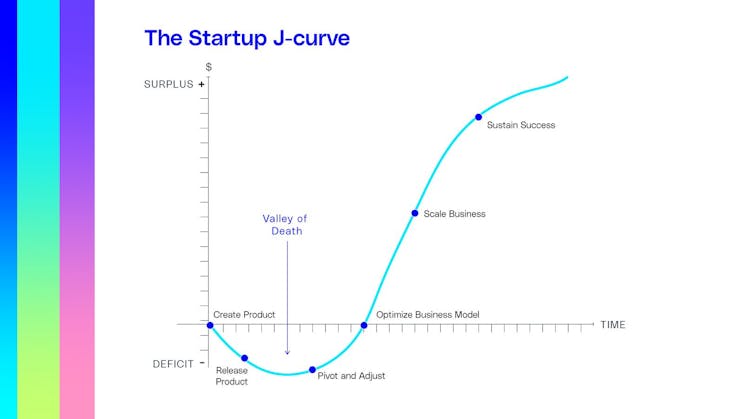

スタートアップ企業の「死の谷」曲線とは何ですか?

死の谷曲線(別名:死の谷)とは、スタートアップ企業が事業を開始したものの、顧客からの収益をまだ上げていない期間を指します。企業がスタートアップ曲線に長く留まるほど、資金の燃焼率が高くなるため、失敗する可能性が高くなります。結局のところ、新規企業が利益を生み出さずに資金を消費する速度が速ければ速いほど、存続期間は短くなるのです。

企業がスタートアップの「死の谷」を乗り越える軌跡は、業界と事業計画の両方に左右されます。例えば、ほとんどのソフトウェアテクノロジー企業は、初期の損失の後、急激な成長を示す有名なJカーブの傾向線を経験します。市場への参入に苦戦する若いスタートアップは、通常、突然の急降下に直面します。事業が勢いを増し、市場への適合性を磨くと、成長の道のりは緩やかな上昇へと変化します。

スタートアップ企業のJカーブにおける典型的な段階

しかし、他の業種では成功への道が必ずしも平坦とは限りません。例えば、気候変動対策技術のスタートアップ企業は、製品開発段階、市場検証段階、そして信頼性を確立する段階の4回にわたって「死の谷」に直面します。どの業界であっても、企業がこの難局を乗り越えるために習得できる重要なステップがいくつかあります。

スタートアップがデスバレーを克服する方法7ステップ)

初期段階では、多くのスタートアップはターゲットオーディエンスを絞り込み、初期資本を構築し、さらには複数の資金源を確保するのに苦労します。 これらの課題はスタートアップ企業の「死の谷」に典型的なものだが、すべてが失われたわけではない。適切な安全策を講じれば、健全な予算を維持しながら、会社の発展に投資することができます。

創業初日から会社の成功確率を高める方法をご紹介します。

1 。最小限の実行可能な製品(MVP)を用いて、製品と市場の適合性を判断する。

研究開発段階において、消費者の購買プロセスにおける最初のステップは何でしょうか?あなたの製品やサービスが、人々が欲しがるもの、あるいは必要とするものかどうかを判断する。市場調査を実施し、十分な資金を確保し、顧客調査を行うことで、自社製品が特定の市場に適合していることを実証しましょう。

最小限の実行可能な製品はテクノロジーのプロトタイプではなく、ターゲットオーディエンスやベンチャーキャピタルのリーダーに対する販売価値を検証するためにビジネスアイデアをテストする方法です。まずは、チームが最小限の労力で実証済みの顧客知識を最大限に調達できるバージョンの製品を導入することから始めます。

2 。多様なスタートアップ資金を模索する。

キャッシュフローはスタートアップにとって大きな課題です。実際、スタートアップの58 % は、スタートアップ段階で自由に使える資金が USD 25 、 000未満です。強力な投資基盤には、会社の発展に投資しながら堅実な予算を維持する明確なビジネスモデルが含まれます。会社の財務上の安全性を最大限に高めるために、必ず複数の資金源から資金を調達してください。

ベンチャーキャピタリストと提携したり、エンジェル投資家と協力したり、政府や組織からの助成金を探したりする。オンライン投資プラットフォームを検討してみましょう。これらは現代的なクラウドファンディングソリューションであり、革新的な事業や潜在的な投資機会のためのダイナミックな場を提供します。より安全なソリューションをお探しですか?さらなる支援を得るために、インキュベーター企業との提携を検討してみてください。

3 。人工知能 (AI) を活用して迅速に拡張します。

テクノロジーはビジネスをより効率的にする鍵であり、人工知能 (AI) テクノロジーは、企業が新しい市場に参入し、世界的に規模を拡大する方法にすでに大きな影響を与えています。適切なソリューションを導入すると、採用、入社プロセス、給与計算、その他のビジネス ニーズを効率化できます。

労働力管理の改善からコミュニケーションの促進まで、人工知能 (AI) はコラボレーションの強化、人工知能 (AI) が生成したコンテンツによるマーケティング ワークフローの合理化、さらにはウィジェットを介したオンライン コミュニケーションの自動化による顧客獲得の向上に役立ちます。

4 。どこでも雇って成長を促進 平等な機会を世界中のすべての人へ。

新たな市場への進出は、最終的に収益の増加と長期的な成功の可能性を高めることにつながります。自問自答してみましょう。あなたの成長目標は何ですか?

グローバル成長は、市場機会を拡大し、競合他社よりも先に顧客を引き付け、多様な 人材プールを開放し、あらゆる仕事に最適な人材を見つけるお手伝いをします。どこから始めればよいか分からない? G-Pでは、10年以上にわたり、企業がシームレスに あらゆる場所のあらゆる人を、企業形態に関係なく採用できるよう支援してきました。初期段階のスタートアップから大規模企業まで、完全にカスタマイズ可能なグローバル雇用製品スイートは、次のステップが何であれ、成長を加速するように設計されています。

5 。チーム作りは慎重に行いましょう。

強力なチームを構築することは非常に重要です。スタートアップ企業の23 %は、チーム組織の不備が原因で失敗しています。会社がまだ成長の停滞期にあるときに採用活動を行う場合は、まず経営陣から始め、リソースが許す限り下位の人材を採用していくのが良いでしょう。一般的に、スタートアップ企業は、複数の責任を柔軟に引き受け、プレッシャーの中でも問題解決に取り組み、会社のミッションを体現できる人材を探すべきです。

スタートアップ企業の創業者は最高経営責任者(CEO)や最高情報責任者(CIO)の役割を担うことが多いが、以下のような他の役割を担う有能な人材を見つける必要がある。

- プロダクトマネージャー

- 営業マネージャー

- ビジネス開発マネージャー

- 最高技術責任者

- 最高マーケティング責任者

- カスタマーサービス担当者

覚えておいてください。ビジネスの成長に伴い、ニーズは変化します。成功への道を切り開くチームを構築するためには、最初の重要な人材を確実に採用する必要があります。過去とは異なり、人材が集まる場所で起業する必要はない。G-Pのような成長の専門家のサポートがあれば、スタートアップ企業は世界中のどこからでも、創業当初からグローバルな視点でチームについて考えることができます。

6 。雇用代行業者(EOR)と提携。

雇用代行業者(EOR)と提携することで、特に国際市場に進出する場合、スタートアップの成長を促進できます。では、雇用代行業者(EOR)とは何でしょうか。また、雇用代行業者(EOR)と提携するメリットは何でしょうか?雇用代行業者(EOR)は、お客様に代わって労働者を合法的に雇用し、人事、人事部、法的複雑さを処理してくれるため、お客様はチームの日常の責任とビジネスの成長に集中できます。

創業者は自分のアイデアを実装し、製品と市場の適合性を達成することに最も関心を持っていますが、多くの場合、採用プロセス、給与計算、契約、現地の労働法、税務コンプライアンスに対処するための帯域幅がほとんどありません。 G-PのようなEOR(雇用代行)の専門知識とサービスを活用すれば、法人形態に関わらず、わずか数分でグローバルな採用を開始できます。

7 。事前に計画を立てる努力をしましょう。

スタートアップ成功のための最後の秘訣とは?財政面でも運営面でも、あらゆる事態に備えておくこと。多様なバックグラウンドを持つグローバルチームを採用して、リソースを拡大しましょう。

経験豊富なチームと共に、事業が「死の谷」と呼ばれる成長曲線における潜在的な損失を緩和するのに十分な資金を調達していることを確認することが不可欠です。しかし、 33 %の スタートアップ企業の資本レベルは10 、 000米ドル以下です。あらゆる業種で予算が限られているため、企業にはほとんどミスの余地がなく、成功の可能性が制限されます。そのため、適切な資金で正しい方法で事業を始めることが非常に重要です。

業界に関わらず、一般的には予算よりも多くの資金を調達するのが最善策です。市場は常に変化しており、未来は予測不可能である。

G-Pで時代の最先端を走り続けよう。

代行(EOR)カテゴリーのリーダーとして認められている当社は、新しい時代のための新しいテクノロジーで道を切り開き続けています。当社の グローバル成長プラットフォームは、 あらゆる段階の企業が必要とするすべてを提供し、180 か国以上でグローバルチームを迅速かつコンプライアンスに準拠して見つけ、管理することができます。 明日の「デスバレー」を突破するために当社がどのように役立つかについて詳しく知りたい場合は、今すぐ 提案をご依頼ください 。